Navigating the New Personal Income Tax Landscape for FY 2025-26

The Union Budget for the Financial Year 2025-26 has introduced significant changes to the personal income tax structure, primarily focusing on making the New Tax Regime more attractive for taxpayers. These amendments are designed to provide substantial relief to the middle class and simplify the tax filing process.

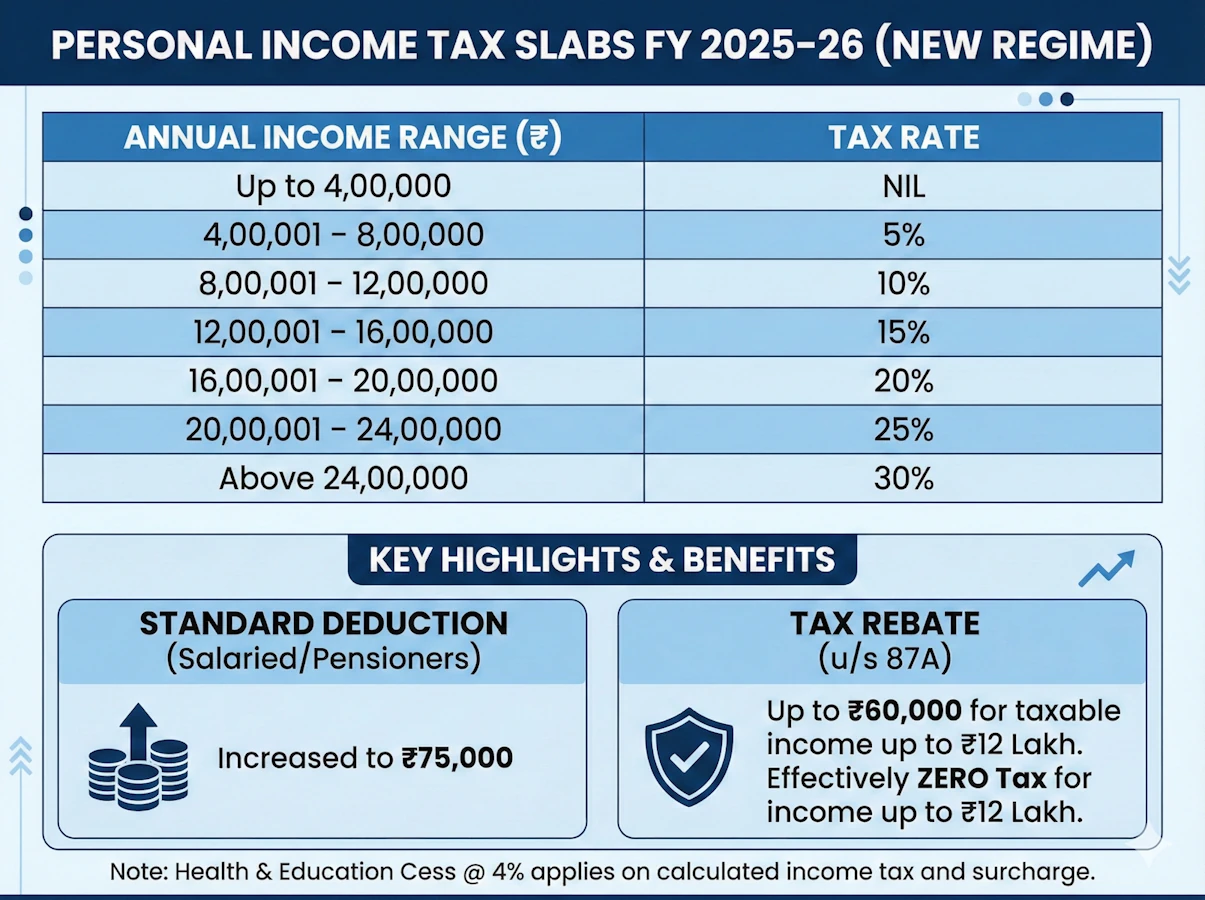

Here is a detailed breakdown of the key highlights and benefits under the new regime that you should be aware of for the upcoming assessment year.

Key Highlights for FY 2025-26 (New Regime)

Zero Tax Threshold up to ₹12 Lakh: One of the most significant updates is the enhancement of the rebate under Section 87A. Individuals with a taxable income of up to ₹12 lakh will now pay zero income tax. This is achieved through a tax rebate of ₹60,000, which effectively nullifies the tax liability calculated on income up to this limit.

Increased Benefit for Salaried Individuals: For salaried taxpayers and pensioners, the benefit is even further extended. With the standard deduction being increased to ₹75,000, a salaried individual earning a gross income of up to ₹12.75 lakh will have a taxable income of ₹12 lakh after the deduction. Consequently, they will fall under the zero-tax bracket due to the Section 87A rebate.

Surcharges and Relief: The highest surcharge under the New Tax Regime is now capped at 25% for incomes exceeding ₹2 crore, providing relief compared to the 37% surcharge in the Old Regime for higher brackets. Additionally, Marginal Relief is available to ensure that if your income slightly exceeds the ₹12 lakh threshold, your tax liability doesn’t jump disproportionately.

Senior Citizen Benefits: The TDS threshold for interest income for senior citizens has been increased to ₹1 lakh, simplifying tax compliance for retirees.

Health & Education Cess: A flat 4% cess continues to apply to the total tax and surcharge liability across both regimes.

Conclusion

While the FY 2025-26 changes make the New Tax Regime highly attractive, the “best” choice remains highly individual. Depending on your existing investments, home loans, and insurance, the Old Regime might still offer advantages in specific cases.

To ensure you choose the most tax-efficient path and maximize your savings, we recommend a personalized consultation. Contact our experts at Ehtesham & Co. to plan your tax strategy for the upcoming year.